Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Tax Filing 2024: For the upcoming filing season, starting on January 29th, taxpayers should be aware of certain aspects. Last year marked the end of pandemic-related tax breaks and a return to pre-COVID levels for popular credits such as the earned income tax credit and child tax credit.

Additionally, taxpayers faced challenges with the IRS’s paper backlog and uncertainties regarding reporting payments from platforms like Venmo and PayPal. However, the previous tax season was relatively more typical, resembling a return to normalcy.

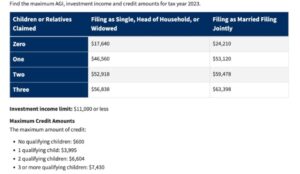

Credit amounts for minors and other dependents.

In the previous year, taxpayers experienced the elimination of pandemic-related tax breaks and a return to pre-COVID levels for popular credits such as the earned income tax credit and child tax credit.

Apart from the IRS’s paper backlog and the confusion surrounding reporting payments from apps like Venmo and PayPal, the last tax season was more aligned with normalcy.

To prepare for this filing season, which commences on Jan. 29, here are some important details to keep in mind.

Credit amounts for children and other dependents:

For the 2023 tax year, the child tax credit (CTC) remains at $2,000 per child (or qualifying dependent) and is partially refundable. This means that if the credit exceeds the tax owed, taxpayers will not receive the full amount.

The other dependent care (ODC) credit is designed for older children and aging parents who are dependents but do not qualify for the child tax credit. The maximum value of this credit is $500.

The earned income tax credit (EITC), which provides tax relief for low- and moderate-income families, has been adjusted for inflation. As a result, there is an increase in the maximum credit amount for families with three or more children, now reaching up to $7,430.

Tax implications of student loan interest deduction and loan forgiveness.

According to Kathy Pickering, chief tax officer at H&R Block, individuals who had to resume their student loan payments in the fall of 2023 may be eligible to deduct a maximum of $2,500 of student loan interest per tax return per tax year.

It is important to note that taxpayers who had their student loans forgiven in 2023 might encounter tax liability.

The American Rescue Plan includes a provision that exempts federal taxes on forgiven student loan debt until 2025. However, if a borrower resides in a state that has not adopted this provision, they may still be responsible for paying state taxes on their forgiven loans.

It is important for taxpayers in Arkansas, Indiana, Mississippi, North Carolina, and Wisconsin to be aware that these states do not conform with the federal tax exemption on student loan forgiveness. Therefore, individuals who had their loans forgiven in these states may be subject to state taxes. To determine their tax obligations, taxpayers should seek guidance from a tax professional.

They can provide information on whether state taxes need to be paid on student loan debt forgiven in the previous year and what documentation, such as a 1099-C, is required from their loan service provider.

Reporting requirements for cryptocurrencies, non-fungible tokens (NFTs), and payment applications.

In the previous year, there was a lot of confusion surrounding the 1099-K reporting requirement. This requirement mandated that third-party payment networks such as PayPal and Venmo send taxpayers Form 1099-K if they received third-party payments for goods and services that exceeded $600. This was a significant change from the previous threshold of $20,000 with over 200 transactions.

The confusion primarily arose from the nature of these transactions. Money received from friends and relatives as personal gifts or for splitting restaurant bills, for instance, did not count as taxable income. However, income tax did apply to goods sold or services provided through a side gig or small business.

To prevent additional confusion, the IRS has once again postponed the implementation of the reduced $600 threshold for the 2023 tax year.

According to Robert Seltzer, a certified public accountant (CPA) at Seltzer Business Management, individuals who are not engaged in legitimate business activities will not be burdened with unnecessary compliance requirements, as he stated in an interview with Yahoo Finance.

In addition to this, taxpayers who conducted transactions involving cryptocurrency and NFTs are also obligated to report their activities. In the previous year, taxpayers were required to answer a question regarding digital assets and disclose any income related to such assets. This year, the question has been rephrased and is applicable to tax returns for trusts and estates as well.

Karla Dennis, an enrolled agent at Karla Dennis & Associates, emphasized the importance of proper reporting to avoid penalties when it comes to transactions involving cryptocurrencies or NFTs. In the event that your digital asset experiences losses, there is an opportunity to deduct some of those losses if you sell the coins. This deduction can help reduce your taxable income and potentially increase your tax refund.

To begin with, these losses can be used to offset any capital gains you may have. If the losses surpass the gains, taxpayers have the ability to deduct up to $3,000 in capital losses per tax year against ordinary earned income, such as wages, salaries, and business income.

Furthermore, the IRS allows taxpayers to carry forward any remaining capital losses indefinitely into the future, with a limit of net $3,000 capital loss per year. This provides individuals with flexibility in utilizing their losses to offset future gains and potentially reduce their tax liability.

Deductions for home offices.

The prevalence of remote work has surged amidst the pandemic, with hybrid work schedules now becoming commonplace.

It is important to note that merely working from home does not automatically grant you the privilege of deducting your home office expenses.

According to Dennis, the home office deduction is typically applicable to self-employed individuals rather than employees. Taxpayers who have transitioned to remote work should be mindful of this distinction.

To be eligible for the deduction, your home office must be used exclusively and regularly for business purposes. This means that if you utilize your dining room table as your workspace but also use it for family meals, you cannot claim this deduction for that particular space.

Tax Day

Tax day marks the beginning of the tax season, which commences on January 29 and concludes on April 15, when taxpayers are required to file their returns.

Nevertheless, residents of Maine or Massachusetts are granted an additional two days to file their taxes, as their deadline is extended to April 17 due to the observance of Patriots’ Day and Emancipation Day.

Furthermore, individuals residing in areas declared as disaster relief zones by the Federal Emergency Management Agency (FEMA) are eligible for an extended deadline. For instance, taxpayers in Connecticut who were affected by the January storms have until June 17 to fulfill their filing obligations.